Buying a house is a big deal. But I think that most people under-invest in making a good decision.

Houses are vastly more expensive and life-affecting than other purchases, so it makes sense to spend vastly more effort to make the right decision. If you want to buy a new dishwasher, you might spend three hours reading reviews and checking them out before you spend £450. In my region the average house price is £450,000, or 1000x more than a dishwasher.1 At the same price/time ratio, you would spend 3000 hours on the decision. Obviously this oversimplifies things (although it implicates many interesting ideas which I’ll leave in a footnote).2 But the core idea is that, due to scope insensitivity, you are likely pre-disposed to under-invest in making this decision relative to other decisions. (I didn’t keep track, but I probably spent 600+ hours over a 6-month period in finding our house.)3

But what should you spend your time thinking about?

Step 1: Should you buy a house?

Before deciding to buy any house, consider whether doing so makes sense. Many people assume that buying a house is always a good financial decision. They point out that (1) rent is often close in cost to mortgage payments, and (2) buying gets you a valuable asset at the end of the day. But this reasoning oversimplifies the relevant variables.

On (1), the cost of rent: the costs of renting vs. buying are highly sensitive to the buy/rent ratio in your local market, (expectations of) interest rates, and transaction costs. (England has a large property transaction tax (‘stamp duty’) which makes short-term ownership very costly.) And, of course, you can compare rental fees vs. repairs/maintenance costs.

On (2), the value of homeowning: there is no iron law that house prices must go up, and a highly leveraged bet only looks good in an appreciating market. Moreover, spending money on a house has opportunity costs: the benefits you could derive from doing something else with that money. Instead of spending on a down-payment and mortgage interest, you could invest that money.4 That investment will grow, just as house value might. And while you haven’t leveraged your bet, you have diversified it.

There are many articles, explainers, and calculators to help you crunch the numbers for your situation. So before deciding to buy, calculate whether it makes sense for you. Don’t be swayed by the cult of homeownership, which pushes people into buying when they would be better off renting.

(Before we bought a house, my partner and I crunched the numbers at length. We predicted that buying was likely to be slightly financially inferior to staying put, but considered it worthwhile on net for non-financial reasons. But we would have changed our mind if buying was far more financially costly.)

Step 2: Where should you buy a house?

Anecdotally, most people seem to pick a location first (near work, school, family, etc.) and then look for a house in that area second. I think that this often results in a worse outcome than if they were more flexible about location, and went back and forth between location and properties to triangulate an optimal mix for their context.

The typical dynamic is that housing is expensive in highly productive cities and cheaper in more rural/unproductive areas. But the efficient market hypothesis doesn’t apply to housing: gains in location desirability do not inexorably incur proportionate price increases.5 Choosing a new location can significantly increase the all things considered desirability of your total location/house package.

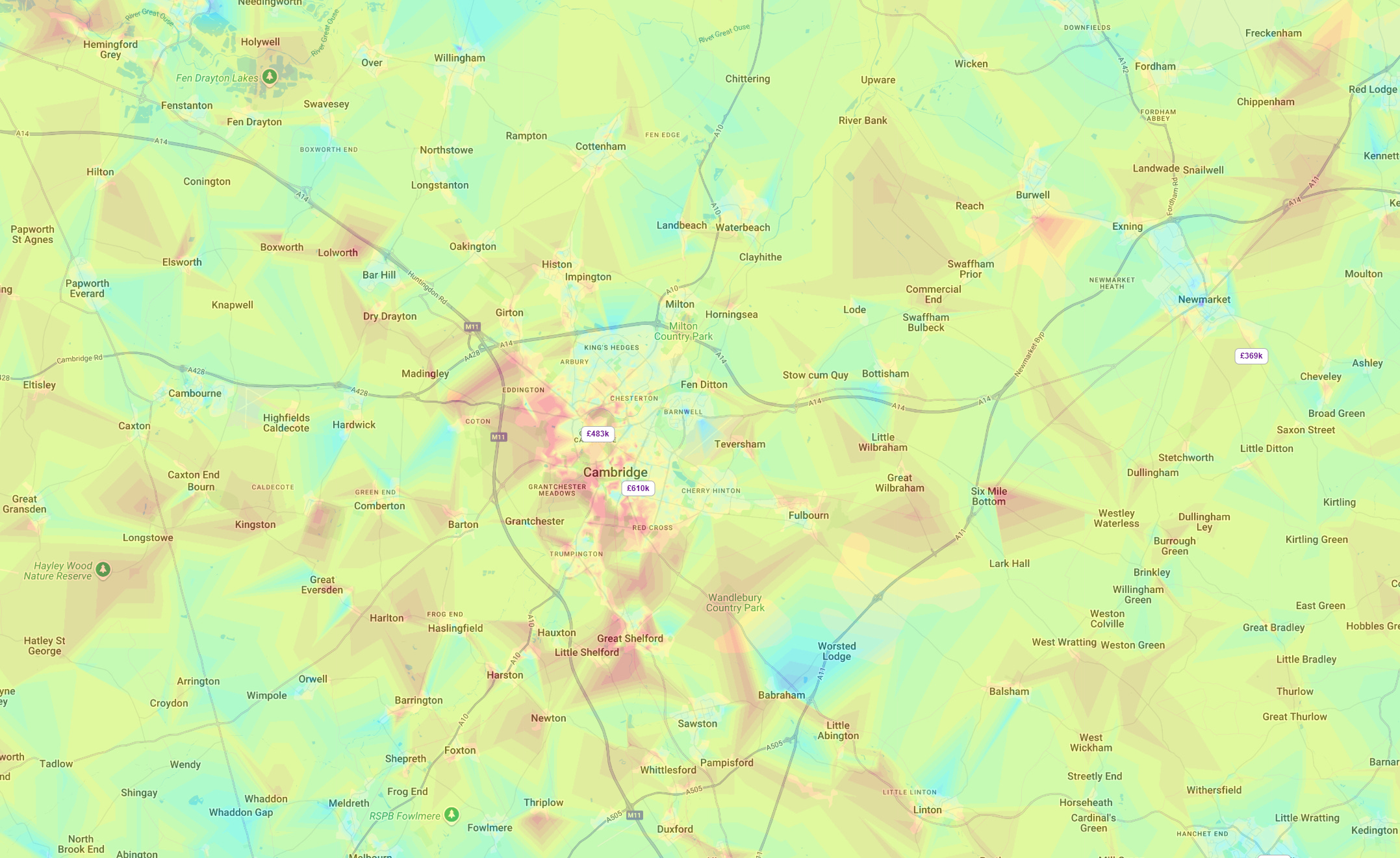

Heatmaps can help you figure out local prices:

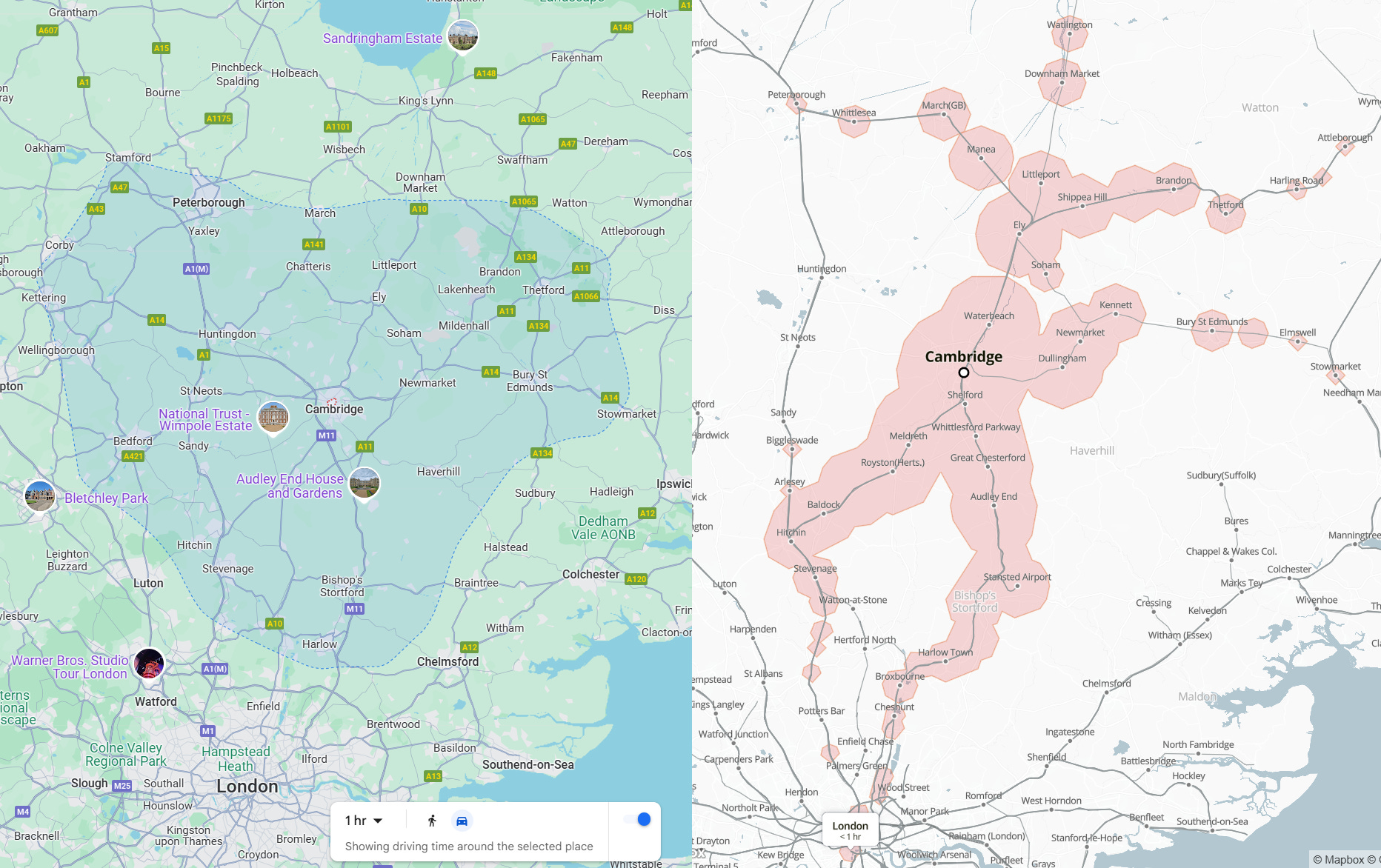

Isochrone (ie travel-time) maps can help you determine commutable distances:

Combining these, you might find places which are equally commutable yet very differently priced. In Cambridge, housing is often (but not invariably) much cheaper out of the city, and villages to the north are cheaper than villages to the south (because the south enters London’s orbit). So if you work in Cambridge and want more house for your money, you should look north of the city.

What does this look like in practice? Well, this 95 sqm terrace is a 15-minute walk from Cambridge town centre and is on the market for £700,000 (no, academics cannot afford this):

But if you are willing to drive 45 minutes north of the city, to Chatteris, your £700,000 could instead buy this 100 sqm detached house with a 5-acre equestrian plot and 200 sqm of outbuildings:

I’m not claiming that the horse house is better. If you prefer cities and walkability then the first will suit you much better. Nor am I claiming that it’s some great insight that rural areas are cheaper than productive cities. Nor am I claiming that commute-distance and cost are the only relevant factors in picking a location: obviously neighbourhood character, amenities, schools, etc, are important.

What I am claiming is that people often underappreciate the extent of variation in price and housing within a reasonable range. You don’t have to move to Wales to get much more property. And you can discover this very quickly, by spending a couple of hours mapping out the possibilities. (I’ve talked to several people buying a house near Cambridge who’d never heard of Chatteris, and thus had no idea what kind of value proposition it represented.)

(It’s a nightmare to drive in central Cambridge, but we do have a park-and-ride system, and I’m bullish on e-bikes and e-scooters opening up an effective and efficient range of commutable distances.)

Before buying I searched a huge range of locations, ranging from London to Lincolnshire, in search of an optimal price/performance ratio for our circumstances. Without doing this, we likely would have bought in a very dodgy part of London rather than a more suitable and very pleasant Cambridgeshire village, and would have paid much more for the privilege.

Step 3: When should you buy a house?

Buy in winter.

I used to sell second-hand clothes, and, predictably enough, there was higher demand for winter clothing in winter, and summer clothing in summer. So if you plan to sell your old clothes, try holding on to those shorts until the summer. Conversely, if you want to buy second-hand clothes, try buying summer gear in winter.

Strangely, a similar seasonal pattern affects houses too. House prices are predictably higher in summer than in winter.6

We started looking for houses in August. It was hard to get viewings, and houses were selling or going to final bids in days or weeks, with many bidders pushing up prices. We finished our search in December, when estate agents would call us to drum up interest.

People often want to be in situ by Christmas. But, given the enormous cost of houses, saving a few percentage points translates into enormous savings. Christmas isn’t worth it. Others want to be in situ for the school year (starting September). That is more defensible. But if that isn’t a deal-breaker for you, then arbitrage the low-demand periods.

This all helps first-time buyers, but what if you’re selling and buying in a chain? Wouldn’t the benefit of a lower purchase price get offset by a lower selling price? Not if you’re upgrading to a more expensive house. Then a fixed percentage point drop helps you much more than a gain. (But vice versa for downsizers.) Indeed, depending on your situation, you might be able to agree a sale in summer but a purchase in winter, to get the best of both worlds. (We managed this by accident.)

Step 4: How should you pick a house?

You’ve decided to buy a house, and narrowed down some good locations. How do you pick a specific house?

Most people seem to browse through property sites, pick out a few houses which look nice within their budget, and then visit them. They then do further viewings for houses they really like and bid on their favourite based on the vibes they get.

The biggest things I did differently were to search (1) more quantitatively and (2) more broadly.

(1) Quantification

I used a spreadsheet to keep track of key data about houses of interest: price, precise location, floorspace, garden area, number of beds and bathrooms, house type (terrace/semi/detached), commute time, road type (1 for quietest, 5 for loudest).

Some of this I could simply copy/paste from listings. Other data I had to find for myself. In England, most listings (bizarrely) do not tell you the precise location (only the street) nor the overall plot size. But this is important info! I saw some apparently great houses on listings which didn’t mention that the house was wedged next to train tracks or abutted a major road - viewing them would have been a waste of time for me. In many countries it’s standard or even mandatory to provide this info in listings. But, given English backwardness, I had to use Google maps to find precise locations and to map plot sizes.

The reason I cared so much about quantifying house and plot size was (a) they’re important, and (b) because you can get a very misleading impression from viewings.

How big a space appears is often determined by how effectively (and densely) it is filled. An empty or sparsely decorated room will feel smaller than well-decorated room. A featureless lawn will feel smaller than a mature garden:

The key reason to quantify these metrics is to avoid being overawed by ephemera and instead to focus on the fundamentals. The vibe you get from a house is often highly dependent on things you are not buying, like the present owners’ décor or gardening skills. (North American realtors seem to appreciate this more than English estate agents, and commonly ‘stage’ the house with temporary furnishings to make it look better.) You can always redecorate a room or plant up a garden. Extending your house or garden are far costlier or impossible.

Once you have a spreadsheet, you can do basic functions like sorting or conditional formatting to more easily spot properties which stand out on some metrics. We found several properties with much bigger gardens than was typical for their price bracket, in part, I think, because English listings simply do not quantify this. (Even in the outdoors-obsessed Covid market.)

The point is not to quantify everything and then simply pick whatever property does ‘best’ on some aggregate metric. (Although you could!) The point is instead to use data to prioritise and focus your search.

The house we ultimately bought did not strike me as particularly interesting from its listing. But it scored well on all my metrics, and turned out to meet our requirements far better than other places which looked more attractive or charming at a glance.

(2) Breadth

I’ve heard many stories of people buying the first house they viewed. What was the probability of it being close to optimal for them? Very low, I suspect, unless they had very specific preferences.7 The much more likely explanation, I think, is that they were excited about buying a house, the first one they saw seemed good enough, and so they offered for it without considering how much better they could do. They saw the explore/exploit trade-off and just mashed the exploit button. I’m not gonna judge, but I think you can do better.

The modern search process has two stages: online research, then viewings.

My sense is that, for most people, the viewing stage is the ‘real’ search. By contrast, I think that the online filter is far more important.

The online search is more important because it can cover far more ground, more efficiently. And a wide search space is important when houses vary across many dimensions. From my online search, I ultimately put around 700 houses into my spreadsheet. This is not every listing I read: I skimmed at least 10x this number. No, those were just the houses of potential interest.

One reason why this number is so high is because I looked at many different areas, and was open-minded as to features. Another reason was that I looked at properties both above and ‘below’ my price range.8 But the biggest reason was simply that I put in a lot of effort to survey the field. By doing this I got a feel for the entire market. At the time you could show me a picture of a house within 10 miles of Cambridge and I could give you its market value within 10%. This allowed me to identify under-priced properties. These properties did tend to get noticed by others, and ‘bid up’ closer to prevailing market rates. But not uniformly and consistently.9 The wider your search area, the more needles you can pull from the haystack. I don’t think this is some difficult skill, and if you’re searching locally then you probably already have a good sense of the market. But it seems easily worth the effort, given the scale of the decision.

But doesn’t a spreadsheet miss out on the stuff that really matters? Don’t you need to a view a house to really get a feel for it? In my experience: no, not really.

In most places in England you can view satellite imagery and go for a street-map walking tour around the neighbourhood, all from the comfort of a browser. With my quantified spreadsheet and some online snooping I already had an excellent sense of the local neighbourhood and quirks of each property before I viewed it. While I only viewed about 15 properties in person, in no viewing did I acquire any especially valuable information which I hadn’t already gleaned online. (And these weren’t generic new builds: they ranged from urban core to countryside, cramped terraces to sprawling farmhouses, centuries-old to mid-20th century.) And, indeed, I put my money where my mouth was: I didn’t do a second viewing, because it wouldn’t have revealed anything new. (Plus, Covid regulations made it a huge hassle.)

(A moment that stuck with me from motorcycle training: if you have to check the same stretch of road twice in quick succession, then you didn’t really check it properly the first time.)

Step 5: How should you seal the deal?

You’ve pinned down a property. How do you go about buying it?

There’s loads of sensible advice out there about how to handle the transaction, advice to which I have nothing to add. Most obviously, you shouldn’t get into a bidding war and pay over the odds: have a firm upper limit and stick to it. (We unsuccessfully bid on several houses by doing this.)

There is, however, a piece of advice which seems mistaken to me. Once you’re serious about a house and have an offer accepted, the standard practice is to commission a home survey to reveal any issues with the property. These cost around £300 to £1500, depending on their scope. I think that these surveys are typically pointless.

The standard reasoning is that a survey is worth the cost because it might uncover hidden problems and therefore allow you to back out of a bad deal or negotiate a better price.

But will a survey uncover hidden problems? For cheaper surveys, probably not. They basically amount to a visual inspection of the house. And while a surveyor has visually inspected more houses than you, they don’t see anything that you can’t see with your own eyes. (You can find many surveyor walk-throughs on Youtube to verify this.) More expensive surveys involve a bit more than a mere visual inspection, but, frankly, not much more. And the information they report is typically so vague and hedged that its value is negligible. (Their standard contractual boilerplate also typically disclaims liability for missing issues.) I don’t think that info is worth very much.

Still, let’s say that your surveyor does uncover something you didn’t spot. Will you back out of the deal as a result? Probably not. If the issue was so glaring that the surveyor confidently declared that it would cost a lot to fix (in a more expensive report), then the seller probably already knew it, and it was already factored into the house price. (Truly deal-breaking issues are very rare.)

Can you at least negotiate a price reduction? Well, you just put an offer on a house and then spent several hundreds of pounds or more commissioning a survey about it. You’re not going to survey lots of homes: that would get very expensive very quickly. So getting the survey is a very strong signal that you want to buy this particular house. Plus, if you’re in a chain, your own sale might collapse if you back out. This puts the buyer in a very strong negotiating position. They have no obligation to lower the price to account for the issues revealed by your survey. They can Just Say No to your requested price reduction. Are you really going to back out, having spent all that money on the survey already? Unlikely.

If surveys are so useless, why does everyone commission them? Mostly, I think that people don’t appreciate how little information they provide beyond what you can see with your own eyes. Further, there’s weak market feedback. It’s hard to assess what counts as a good survey, so you get a market for lemons. (It’s not like personal home buyers are going to be repeat customers.) A further reason is that the price seems cheap relative to the house price. But the fact that something is a small component of a very big expenditure doesn’t mean that you should lose your head about the value of that component.

Conclusion

What have we learned? In short: I think that most people should think harder about whether to buy a house, where to buy, when to buy, how to find one to buy, and how to actually buy it. That’s annoying, but it’s worth it for the biggest purchase that most people will ever make.

Appendix on Interesting Legal Issues about Surveys

Instead of buyers individually paying to commission home surveys on homes they don’t own and have no guarantee of purchasing, it would be far more sensible/efficient for sellers to commission their own survey and then advertise the results to all potential buyers. Just as manufacturers give warranties to signal faith in their product’s reliability, a (positive) seller-commissioned survey would give a strong signal of house reliability. I’m puzzled why this isn’t standard practice.

Part of the reason, perhaps, is that surveyors would enter contractual relations only with the seller, not the buyer, and so buyers could not legally rely on those assurances as they are not a party to the contract. Surveyors would therefore be incentivised to whitewash the results, as this would benefit their client, the seller, at the expense of third-party buyers.

I don’t think that most buyers would really think through the contractual incentives here and so I don’t see this as an overwhelming reason against seller-commissioned surveys. (Though a vague sense of surveys being whitewash exercises might percolate through to general consciousness). But, while we’re here, it reminds me that this situation gives rise to an interesting issue in English law.

Mortgage providers also perform their own (watered down) surveys before providing mortgages. These surveys are often relied upon by buyers. But, as noted, there is only a contract between the surveyor and the bank. The surveyor has no contractual relation with the buyer. So if the surveyor messes up the survey, and the buyer relies on it to their detriment, that buyer would not have any remedy available in contract.

But English stretched a different area of law—the tort of negligence—to provide a remedy for third-party buyers in this kind of situation.

Some background: the tort of negligence requires D to compensate C if D negligently caused C foreseeable actionable losses, providing that D owed a duty of care not to cause such losses to C. Importantly, these duties are not generated via contracts. For example, we all have a general duty not to cause each other physical harm through physical carelessness. (If you carelessly knock over my ladder and cause me to fall off and get injured, then I can sue you for compensation.) Specialised roles also come with specialised duties (eg doctor/patient, lawyer/client).

However, there is no general duty not to cause economic losses to others, outside of limited situations where A provides information to B and B reasonably relies on it to their detriment. (If I wrongly advise you not to buy a Macbook when actually you’d benefit from one, Apple can’t sue me for causing them lost custom.)

Back to surveys. If a surveyor works for a mortgage lender, they owe a duty to that mortgage lender to do a good job. (This duty arises in contract law, but it also fulfils the conditions in the previous paragraph to give rise to a duty in tort law.) But the surveyor is not providing information to the buyer, even though the buyer relies on it, and so no duty arises to the buyer in contract or in tort.

Despite this, in a (highly dubious) leading case, the House of Lords decided that mortgage surveyors do sometimes owe a duty of care to third-party home-buyers who (reasonably) rely on these surveys. This meant that surveyors could suddenly be sued by a much larger group of potential claimants, without any contractual compensation for incurring that broader risk.

If I were a (well-advised) surveyor, I would therefore be very wary about permitting my surveys to be viewed by third parties. And I would be careful to make the information provided vague and legally defensible, lest I get challenged on it years down the line, by any number of subsequent buyers.

Perhaps cognisant of some of these pitfalls, the Court of Appeal more recently distinguished the earlier case, and refused to find that a surveyor owed a duty of care to a commercial landlord who relied on a mortgage survey, for it was not reasonable for such a commercial operator to rely on a third-party survey. They should commission their own if they to rely on it with the force of law.

But, with all that said, I have no idea whether any of this legal wrangling actually affected how surveyors go about their business.

In fact the total house cost will be much higher due to mortgage interest.

You could search ‘dishwasher’ and buy the top hit in 10 minutes. But that dishwasher is probably suboptimal in terms of price/performance/compatibility relative to dishwashers you could buy after more careful thought. More information/searching would help you make a better decision. But that searching costs you time, and so you need to balance the performance gain against the time cost. So you want have an idea about the value of information (and the value of your time).

When I researched this, most dishwashers seemed pretty similar, so the value of information about any particular model is low. (There is no industry-standard ‘washing quality index’, so it’s basically impossible to compare dishwashers on the only metric that I really care about. Still, this famous Youtube video suggests that most dishwashers are basically similarly good at dishwashing.

So maybe it’s overkill to spend 3 hours researching dishwashers. But did you know in advance that most dishwashers are pretty similar? If not, you’d have to figure that out before deciding how long to spend on object-level research about dishwasher differences. And so now you have two value of information puzzles to solve.

Moreover, you’re not going to be certain in your answers to either question, so you need to make a decision under uncertainty, and decide where to land on the explore/exploit trade-off. All of this now sounds pretty complex and mathematically challenging, so maybe you rely on some simple heuristics. But wasn’t Kahneman and Tversky’s famous paper subtitled ‘heuristics and biases’? And don’t you want to avoid those biases? But how can you do that without a load of cognitive effort?

The latest edition of the American Economic Review has a paper claiming that most of the biases which arise in classic uncertainty scenarios are not in fact driven by uncertainty, but rather by complexity per se (paper, Noah Smith summary). And you just wanted to buy a dishwasher!

Another way to think about this: if my time is worth £20/hour, 600 hours is £12,000 of search cost, or 2.6% of my area-average house cost (£450k). But the 3 hours looking up dishwashers costs £60, or 13% of the dishwasher cost (£450).

If in doubt, invest in low-fee, diversified tracker funds, eg from Vanguard or Blackrock.

To elaborate: if Apple stock was for some reason under-valued, then Goldman Sachs would buy Apple stock in vast quantities until it was ‘correctly’ priced. So if you think AAPL is undervalued, the best explanation for this is that you are wrong. It is correctly valued. This is (one version of) the efficient market hypothesis.

But the efficient market hypothesis doesn’t apply to housing. There isn’t a deep pool of smart money waiting to buy up under-priced houses until they are correctly valued. There’s no way to short-sell over-priced houses. And everyone has a different bundle of preferences as to what they want in a house. This suggests that you can beat the market.

While I agree - this post would be pointless otherwise - in practice I found the market to be sufficiently deep and liquid that there were no truly amazing bargains within my search parameters, or at least not any without corresponding risks (eg cash only auctions). There are still enough buyers to sniff out and bid up true steals.

Here’s a 96-page academic paper on the topic. One great thing about blogging as opposed to academic writing is that I don’t have to read the stuff I cite.

A possible exception is if they wanted a new build in a specific area, as those tend to be rare in England, and pretty uniform.

Looking at prices above your range is a good idea to get a sense of potential price ceilings or movement: looking more expensive properties can give you a sense of whether yours could hit that range with some work/luck. Looking ‘below’ your range can tell you whether you really need to spend more to satisfy your conditions.

Estate agents are rationally incentivised to sell a house quickly rather than maximising sale price. So unless buyers resist, a low starting price often means a lower selling price. I’ll say more about this in the sequel to this post, How to Sell a House.